Insider information on Republic Bank...

If I could add my two cents here…. when reviewing the Martin Armstrong situation it's important to note the following:

1)Republic Bank, the securities firm his company traded thru and kept client funds, was in the middle of a merger negotiation for $10 billion with HSBC when the Japanese FSA started investigating Cresvale/PEI. So when the FSA inquired with Republic for confirmation of client funds Republic then started closing positions without PEI/Amstrong approval and then contacted US authorities before Armstrong new what was going on. This resulted in substantial losses, and their objective was clear: make Armstrong the scapegoat and save the merger with HSBC - which they did by knocking off $500 million from their price tag, which ultimately re-surfaced in the form of payment to the supposed victims in Japan a couple of years later when they finally had to admit guilt for mishandling client funds. But by that time it didn’t matter, they already secured their acquisition and Armstrong was already publicly made out to be the villain. $500 million was a small price for them to pay.

2)Although Armstrong flat out admitted being on the wrong side of trades towards the end and losing a sizeable amount of money, that is no crime. Moreover it's inaccurate to reference quotes from those at Republic Bank as a source for Armstrong's trading performance. In particular, the individual who made the quote you reference regarding Armstrong's performance being no better than "flipping a coin" was later found to have been stealing from PEI accounts while working at Republic. The government later found that this individual, along with one colleague at Republic and a senior person at PEI, orchestrated a scheme in which he siphoned winning trades from PEI and allocated them into personal accounts while taking losing trades and putting them into PEI accounts. Hence, he had every reason to tell people Armstrong's trading was much worse than it really was because he himself was taking millions in winning trades. I believe he is coming up for sentencing of his own soon.

3)One final note, what Armstrong recently plead guilty to is a far cry from what he was originally charged with. He admitted to bad trades, shared accountability with Republic for failing to keep client funds segregated from each other, and took responsibility for allowing sales/marketing materials to continue to go out to prospective clients that promoted favorable trading performance even as he/PEI continued to lose money (hence, the “misleading of clients”).

I'm not here to proclaim Armstrong was without fault, he obviously made mistakes and has paid for them, but there is more that meets the eye in his case and there is a big difference between a legitimate, well intentioned business failing and a business the set out to deceive and defraud from the outset. Clearly Armstrong is the former, not the latter, and his research and contributions to the industry (see earlier post about his discovery of 8.6yr cycle) should be recognized independently.

Written by Anonymous from http://nihoncassandra.blogspot.com/2006/08/enigma-of-martin-armstrong.html

Monday, September 25, 2006

Saturday, July 01, 2006

When was the 6th Amendment Repealed?

From: JerseyGOP a now defunct pro-Republican web site advocating small government and upholding law.

AuthorTom Schneider

When was the 6th Amendment Repealed?

"In all criminal prosecutions, the accused shall enjoy the right to a speedy and public trial, by an impartial jury of the state and district wherein the crime shall have been committed, which district shall have been previously ascertained by law, and to be informed of the nature and cause of the accusation; to be confronted with the witnesses against him; to have compulsory process for obtaining witnesses in his favor, and to have the assistance of counsel for his defense."

Amendment VI of the US Constitution

While our Constitution seems to be under constant attack these days form many fronts there is apparently one amendment we surrendered years ago. Currently there is a prominent US businessman who has been held for over two years in prison without a trial, stripped of his assets, and even for a time denied legal counsel.

He was once a darling of the conservative movement, helping the successful launch of The Weekly Standard and Bill Kristol’s career in the media. When The Weekly Standard was on the brink of failure he was the sole advertiser, promoting not his own products and services, but public service announcements supporting a national sales tax. He hosted forums where Kristol spoke alongside dignitaries like Margaret Thatcher. He wrote reports that strengthened the positions of members of congress like Dick Armey, and think tanks like GOPAC. Now that he is imprisoned with fewer rights than those granted to Gihad-Johnnie everyone seems to have forgotten him and the Sixth Amendment.

Martin Armstrong was once the founder and head of The Princeton Economic Institute, in Princeton, NJ. There he did historical and current market analysis and wrote monthly reports on economic and political trends. He was incarcerated on Jan. 14, 2000 accused of defrauding Japanese investors out of $1 billion. He was once free on $5 million bond after pleading innocent and having his and his children’s possessions confiscated. The $1 billion number was gradually lowered to half of that, but still there is no trial date.

The judge believes he is hiding assets and that keeping him locked up indefinitely will cause him to turn these supposed assets over and admit guilt. This is not the way the American justice system is supposed to work. This is the kind of treatment Amnesty International protests in China. This is the way justice was carried out in communist Russia.

Today the First Amendment is under attack by Democrats and Republicans alike with Campaign Finance Reform, the Fourth by high-tech surveillance systems and national ID cards, and the Second by the usual suspects. Do any of these components of The Bill of Rights stand a chance at survival if we ignore the actual elimination of the Sixth? If our leaders will not stand up for the Constitutional rights of their supporters and political warriors, can the rest of us; not a part of the political game, have any hope of anyone defending our rights?

In this case not only is the sixth Amendment being violated but probably the Fifth, Seventh, and Eighth, as well. If the state cannot convict and is unwilling to even try then the accused remains innocent in the eyes of law and should not be imprisoned or have assets confiscated.

"There is surely a limit to how long someone will choose to stay in jail, even for $14.9 million," the appeals court said. And then added, "The length of his confinement must be viewed in the light of the value of the concealed property, which is unusually great."

If there is no proof of guilt then the numbers presented in the allegations should be meaningless. American Justice must be blind to class as much as it is to race.

The Associated Press reported that, "The court said in an eight-page ruling that Armstrong's repeated efforts to overturn the incarceration order by U.S. District Judge Richard Owen probably had weakened its coercive effect."

This is a blatant warning to all citizens not to challenge the authority of judges. It is a threat against US citizens asserting their constitutional rights. It is an insult to our system of government and stinks of bias and corruption.

If a person can receive additional punishment for simply annoying a judge by asserting Constitutional rights, doesn’t that approach ‘cruel and unusual punishment’?

Armstrong was first held on a contempt order that expired after 18 months. A newly issued contempt order last July 6 has no set expiration date. The court has now said that, "Armstrong will for the first time be faced with the prospect of indefinite confinement."

How long can a judge take The US Constitution into his own hands and suspend its authority? How does this coexist with the right to a "speedy and public trial"?

The press had a hissy-fit over the treatment of the terrorist detainees in Gitmo-Bay, in an effort to protect their rights. Where are they when a US citizen is denied rights in our own country? Where is Bill Kristol now? Is Dick Armey too busy planning retirement to defend the constitution and one of the original authors of the national sales tax plan?

Does the US Constitution have any actual meaning or protectors anymore?

AuthorTom Schneider

When was the 6th Amendment Repealed?

"In all criminal prosecutions, the accused shall enjoy the right to a speedy and public trial, by an impartial jury of the state and district wherein the crime shall have been committed, which district shall have been previously ascertained by law, and to be informed of the nature and cause of the accusation; to be confronted with the witnesses against him; to have compulsory process for obtaining witnesses in his favor, and to have the assistance of counsel for his defense."

Amendment VI of the US Constitution

While our Constitution seems to be under constant attack these days form many fronts there is apparently one amendment we surrendered years ago. Currently there is a prominent US businessman who has been held for over two years in prison without a trial, stripped of his assets, and even for a time denied legal counsel.

He was once a darling of the conservative movement, helping the successful launch of The Weekly Standard and Bill Kristol’s career in the media. When The Weekly Standard was on the brink of failure he was the sole advertiser, promoting not his own products and services, but public service announcements supporting a national sales tax. He hosted forums where Kristol spoke alongside dignitaries like Margaret Thatcher. He wrote reports that strengthened the positions of members of congress like Dick Armey, and think tanks like GOPAC. Now that he is imprisoned with fewer rights than those granted to Gihad-Johnnie everyone seems to have forgotten him and the Sixth Amendment.

Martin Armstrong was once the founder and head of The Princeton Economic Institute, in Princeton, NJ. There he did historical and current market analysis and wrote monthly reports on economic and political trends. He was incarcerated on Jan. 14, 2000 accused of defrauding Japanese investors out of $1 billion. He was once free on $5 million bond after pleading innocent and having his and his children’s possessions confiscated. The $1 billion number was gradually lowered to half of that, but still there is no trial date.

The judge believes he is hiding assets and that keeping him locked up indefinitely will cause him to turn these supposed assets over and admit guilt. This is not the way the American justice system is supposed to work. This is the kind of treatment Amnesty International protests in China. This is the way justice was carried out in communist Russia.

Today the First Amendment is under attack by Democrats and Republicans alike with Campaign Finance Reform, the Fourth by high-tech surveillance systems and national ID cards, and the Second by the usual suspects. Do any of these components of The Bill of Rights stand a chance at survival if we ignore the actual elimination of the Sixth? If our leaders will not stand up for the Constitutional rights of their supporters and political warriors, can the rest of us; not a part of the political game, have any hope of anyone defending our rights?

In this case not only is the sixth Amendment being violated but probably the Fifth, Seventh, and Eighth, as well. If the state cannot convict and is unwilling to even try then the accused remains innocent in the eyes of law and should not be imprisoned or have assets confiscated.

"There is surely a limit to how long someone will choose to stay in jail, even for $14.9 million," the appeals court said. And then added, "The length of his confinement must be viewed in the light of the value of the concealed property, which is unusually great."

If there is no proof of guilt then the numbers presented in the allegations should be meaningless. American Justice must be blind to class as much as it is to race.

The Associated Press reported that, "The court said in an eight-page ruling that Armstrong's repeated efforts to overturn the incarceration order by U.S. District Judge Richard Owen probably had weakened its coercive effect."

This is a blatant warning to all citizens not to challenge the authority of judges. It is a threat against US citizens asserting their constitutional rights. It is an insult to our system of government and stinks of bias and corruption.

If a person can receive additional punishment for simply annoying a judge by asserting Constitutional rights, doesn’t that approach ‘cruel and unusual punishment’?

Armstrong was first held on a contempt order that expired after 18 months. A newly issued contempt order last July 6 has no set expiration date. The court has now said that, "Armstrong will for the first time be faced with the prospect of indefinite confinement."

How long can a judge take The US Constitution into his own hands and suspend its authority? How does this coexist with the right to a "speedy and public trial"?

The press had a hissy-fit over the treatment of the terrorist detainees in Gitmo-Bay, in an effort to protect their rights. Where are they when a US citizen is denied rights in our own country? Where is Bill Kristol now? Is Dick Armey too busy planning retirement to defend the constitution and one of the original authors of the national sales tax plan?

Does the US Constitution have any actual meaning or protectors anymore?

Wednesday, June 14, 2006

Princeton Economics Press Release Sept.1999

Press Release of

Princeton Economic Institute September 20, 1999

The Princeton Economic Institute is an independent research organization and is not owned by Martin Armstrong nor is Mr. Armstrong a director of the Institute. It is NOT related to Princeton Global Management or part of Princeton Economics International nor does it engage in the management of any funds.

Our daily forecasting reports, Global Market Watch and system models used at Princeton Economic Institute are independent models that are not the product of any single analyst. It is our intent to continue to publish our research and bring an independent and objective information to our many loyal clients around the world.

While Mr. Armstrong has always been an outspoken opponent against government manipulations, interventions and "the billionare's club", his direct warnings about the political corruption in Japan and the billions of dollars in hidden losses within its financial system , in some cases carried out by ex-MOF officials, have put him in the direct line of fire by the Japanese government as the man they most wish to discredit. No doubt his highly critical stand against the accounting systems used by all governments that falsely distort CPI, GDP, trade statistics, poverty statistics and taxation have not made him very popular in some circles. His outspoken warnings about the failure of the Euro have also created a few enemies. Mr. Armstrong has always been aware that his research has made him a target over the years nevertheless, he has always stood his ground.

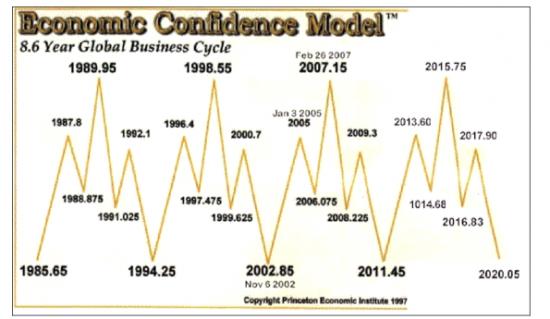

Mr. Armstrong's involvement as an activist in governmental reform is well documented particularly in the field of global tax reform and its impact upon the economy. He stood by his convictions against the birth of the G5 back in 1985. When his Economic Confidence Model pinpointed the precise day for the low during the crash of 1987, he stood alone calling for new highs into1989. His research was even requested by the Brady Commission charged with investigating the incident and some of our clients were on the Commission itself (See Request). He became famous in Japan when his model also projected the high for the Nikkei in 1989 and boldly warned that the market would collapse by 20,000 points within 10 months. His research forewarned of the bull market in US and European equities in 1994 calling for the Dow to reach 6,000 by 1996 and later 10,000 by 1998. (See Vancouver Sun) His research warned of the Asian Crisis in 1997 and of course his model was able to project the collapse of Russia which made headlines in the London FT. His warning that the Euro would fail made him an enemy to some political groups in Europe. Of course when the very same model that pinpointed the 1987 Crash, Tokyo Crash and the birth of the bull market in equities also gave July 20th as an important major top last year, the validity of more than 20 years of his model became undeniable.

As staff members here can attest, even the CIA approached this office requesting that Mr. Armstrong assist the government in duplicating his model just last October, but he refused offering advisory services while insisting that the model remain proprietary. Mr. Armstrong was invited to China by the government where the Chinese made a similar proposal to obtain his model following his successful forecast of the Asian Crisis in 1997. Even after a visit to Princeton in 1998 by a representative of China, Mr. Armstrong still refused to cooperate with the Chinese insisting that the model remain proprietary.

Even the Gold Bugs have tried to join in on the issue claiming that there is a huge short position in gold of 20,000 ounces and that the demise of Mr. Armstrong will now lead to a bull market. Once again, there is no huge short position by anyone and this is another example of outright slander by GATA in a futile attempt to blame Mr. Armstrong for the bear market in gold simply because of his warnings of coming central bank and IMF sales more than one year ahead of the general media. Mr. Armstrong's warning that gold would decline has generated even personal threats sent to this office by some crazy Gold Bugs. There are many who have a vested interest in trying to discredit Mr. Armstrong, including one financial institution in particular which stands a lot to gain. They may all try to kill the messenger, but they will not change the forecasts that he has made for the future.

Mr. Armstrong flatly denies the allegations made against him and he intends to vigorously defend himself. His attorney has stated publicly that he is being made a "scapegoat" but the media prefers to print the propaganda handed directly to them by his opponents. The Japanese press is blaming all foreign firms for the demise of the Japanese financial system and even the FSA has publicly stated that they will investigate all foreign firms in Japan with a new nationalistic zeal after the Credit Swiss affair. If Mr. Armstrong is misquoted by the media in any response he would make, it can be used against him by the government. This is why his legal advisers insist upon his silence until he is heard in a court of law. Any similarity to Credit Swiss has been totally ignored by the western media and they prefer to try to discredit his research of the past 20 years. At no time has Mr. Armstrong ever misrepresented his background as confirmed by Mark Pittman of Bloomberg in his article of September 14, who interviewed him two years ago for Bloomberg. After all, Keynes, Ricardo and even Adam Smith became important contributors to economics without any formal degree in the subject relying instead upon unbiased experience and observation.

The staff of Princeton Economic Institute greatly appreciate the numerous responses of support, the gifts sent to the staff to cheer them up and those who have come forward offering even financial support to insure the long-term survival of this operation. We will keep our clients updated as to any developments in the near future and the staff here will do its best to keep the flame of free speech and objectivity alive. It is not an easy task.

Princeton Economic Institute September 20, 1999

The Princeton Economic Institute is an independent research organization and is not owned by Martin Armstrong nor is Mr. Armstrong a director of the Institute. It is NOT related to Princeton Global Management or part of Princeton Economics International nor does it engage in the management of any funds.

Our daily forecasting reports, Global Market Watch and system models used at Princeton Economic Institute are independent models that are not the product of any single analyst. It is our intent to continue to publish our research and bring an independent and objective information to our many loyal clients around the world.

While Mr. Armstrong has always been an outspoken opponent against government manipulations, interventions and "the billionare's club", his direct warnings about the political corruption in Japan and the billions of dollars in hidden losses within its financial system , in some cases carried out by ex-MOF officials, have put him in the direct line of fire by the Japanese government as the man they most wish to discredit. No doubt his highly critical stand against the accounting systems used by all governments that falsely distort CPI, GDP, trade statistics, poverty statistics and taxation have not made him very popular in some circles. His outspoken warnings about the failure of the Euro have also created a few enemies. Mr. Armstrong has always been aware that his research has made him a target over the years nevertheless, he has always stood his ground.

Mr. Armstrong's involvement as an activist in governmental reform is well documented particularly in the field of global tax reform and its impact upon the economy. He stood by his convictions against the birth of the G5 back in 1985. When his Economic Confidence Model pinpointed the precise day for the low during the crash of 1987, he stood alone calling for new highs into1989. His research was even requested by the Brady Commission charged with investigating the incident and some of our clients were on the Commission itself (See Request). He became famous in Japan when his model also projected the high for the Nikkei in 1989 and boldly warned that the market would collapse by 20,000 points within 10 months. His research forewarned of the bull market in US and European equities in 1994 calling for the Dow to reach 6,000 by 1996 and later 10,000 by 1998. (See Vancouver Sun) His research warned of the Asian Crisis in 1997 and of course his model was able to project the collapse of Russia which made headlines in the London FT. His warning that the Euro would fail made him an enemy to some political groups in Europe. Of course when the very same model that pinpointed the 1987 Crash, Tokyo Crash and the birth of the bull market in equities also gave July 20th as an important major top last year, the validity of more than 20 years of his model became undeniable.

As staff members here can attest, even the CIA approached this office requesting that Mr. Armstrong assist the government in duplicating his model just last October, but he refused offering advisory services while insisting that the model remain proprietary. Mr. Armstrong was invited to China by the government where the Chinese made a similar proposal to obtain his model following his successful forecast of the Asian Crisis in 1997. Even after a visit to Princeton in 1998 by a representative of China, Mr. Armstrong still refused to cooperate with the Chinese insisting that the model remain proprietary.

Even the Gold Bugs have tried to join in on the issue claiming that there is a huge short position in gold of 20,000 ounces and that the demise of Mr. Armstrong will now lead to a bull market. Once again, there is no huge short position by anyone and this is another example of outright slander by GATA in a futile attempt to blame Mr. Armstrong for the bear market in gold simply because of his warnings of coming central bank and IMF sales more than one year ahead of the general media. Mr. Armstrong's warning that gold would decline has generated even personal threats sent to this office by some crazy Gold Bugs. There are many who have a vested interest in trying to discredit Mr. Armstrong, including one financial institution in particular which stands a lot to gain. They may all try to kill the messenger, but they will not change the forecasts that he has made for the future.

Mr. Armstrong flatly denies the allegations made against him and he intends to vigorously defend himself. His attorney has stated publicly that he is being made a "scapegoat" but the media prefers to print the propaganda handed directly to them by his opponents. The Japanese press is blaming all foreign firms for the demise of the Japanese financial system and even the FSA has publicly stated that they will investigate all foreign firms in Japan with a new nationalistic zeal after the Credit Swiss affair. If Mr. Armstrong is misquoted by the media in any response he would make, it can be used against him by the government. This is why his legal advisers insist upon his silence until he is heard in a court of law. Any similarity to Credit Swiss has been totally ignored by the western media and they prefer to try to discredit his research of the past 20 years. At no time has Mr. Armstrong ever misrepresented his background as confirmed by Mark Pittman of Bloomberg in his article of September 14, who interviewed him two years ago for Bloomberg. After all, Keynes, Ricardo and even Adam Smith became important contributors to economics without any formal degree in the subject relying instead upon unbiased experience and observation.

The staff of Princeton Economic Institute greatly appreciate the numerous responses of support, the gifts sent to the staff to cheer them up and those who have come forward offering even financial support to insure the long-term survival of this operation. We will keep our clients updated as to any developments in the near future and the staff here will do its best to keep the flame of free speech and objectivity alive. It is not an easy task.

8.6-Year Review

by Martin A. Armstrong

As a brief introduction to the 8.6-year frequency within the Princeton Economic-Confidence Model, let us follow its course beginning with the last major panic that took place in October 1929 from the US perspective. Factoring in the month of October as .75 to represent a decimal portion of the calendar year, the calculations embark on their journey with 1929.75 to see how well the cycle will hold up in forecasting the past 52 years. The next step was to add 4.3, half the cycle duration, to come up with the next bottom. It projected 1934.05 which would have been January. This year marked the Gold Reserve Act and the beginning of the New Deal. As a result, it also marked the beginning of the turning point in that human emotion known as hope. The stock market had actually bottomed in 1932 and in the later part of 1934 it had begun a rally that would double the Dow Industrials by March of 1937. Continuing on, we apply the next half cycle of 4.3 years which brings us to the next peak projection of 1938.35. This was extremely close to the real events. The stocks had peaked early, a s they always do in a recovery. The long-term trend in the business cycle had rallied from a -38% to -10% in growth according to the Cleveland Trust Co. Index of US business activity. Despite the fact that the growth was still negative, it was a strong improvement within the economy that began to fall off reaching a -18% during 1939. The next bottom, projected out by adding another half cycle of 4.3 years to arrive at 1942.65, which corresponded to the beginning of World War II and another beginning of an economic boom. The Dow Jones Industrials had been declining since March of 1937 when it peaked at 194.40. the Dow eventually bottomed out on April 28th, 1942 at 92.92. From there the Dow would begin another 4 year rally.

The 8.6-year cycle was holding up very nicely. From 1942’s bottom, the cycle peaked again in 1946.95. This corresponded with the end of the World War II period and the beginning of the post war recession. The stock market had peaked during 1946 at the 220 level on the Dow and for the next three years the Dow traded sideways between 160 and 200.

Moving ahead, the next bottom was projected to arrive at 1951.25. The 1949 recession was a deep one in which the US did not begin to pull out until 1951. Although the business cycle began to rise due to the Korean War during mid 1950, it actually peaked during mid 1954 at a +18% on the Cleveland Trust Co. Index followed by a sharp drop to a -2% in 1954. The Dow had started to rise during 1950 and remained in a bull market rising from 195 to reach 525 by 1956.

The next cyclical peak projected out to be 1955.55. The Dow had pulled off a 250% rally between 1950 and 1956 and then fell sharply by 100 points going into 1957. The business cycle peaked during October of 1955 rising from a -2% in 1954 to a +8% growth factor during 1955. The cycle at this point appeared to hold up very nicely, being off no more than 1 year at any point.

From the 1955 projected peak, the next cyclical low was due in 1959.85. The Dow had actually bottomed during 1957. During 1958 and 1959 a bull market once again returned to the Dow Industrials. The business cycle fell from the 1955 high of a +5% to a bottom during 1958 of a -7%. Early during 1959 the business cycle growth bounced back to a +6%, but in the last quarter of 1959 fell again reaching a -1%.

The next peak on the 8.6-year cycle projected out to be 1964.15. During this year, silver coins became extinct and inflation, as measured by the CPI index, had reached 92.9 which was nearly double that of 1929. Industrial production rose in its index that year for the first time to exceed the 80 level after bottoming out during 1932 at 11.6. The Dow was still strong, reaching a high during 1964 near the 890 level only to continue to eventually reach 1001.11 during 1966.

The cyclical projection then called for a bottom on 1968.45. The Dow had peaked on February 9th, 1966 and a sharp 260 point decline had begun. Inflation had continued to mount in much of the world. The United States and six West European nations agreed on March 18th, 1968 to discontinue the sale of gold to private buyers.

The next cyclical projection pointed to a peak in 1972.75. The Dow Industrials had rallied from a sharp decline which saw the Dow bottom at 627.46 on Tuesday, May 26, 1970. From that low, the rally in the Dow peaked at 1,051.70 on January 11, 1973. That high would remain a major record high going into the 1980s. This projection was accurate because the 1973 recession was a serious one, marked by the failure of the Franklin National Bank. It would serve as the worst recession since the 1929 panic.

The next projection came up with a bottom during January 1977.05. The early peak on the Dow during 1973 was followed by a severe panic decline that dropped even below the previous cycle low in the Dow. The bottom came on December 6th, 1974 after nearly a 50% decline. Despite the fact that gold began its rally during August of 1976, the economy didn’t begin its inflationary upswing until 1977.

The next projected high on this 8.6-year cycle called for that peak to come in at 1981.35. This was the precise month when the bond market reached a bottom and interest rates began to turn downward. But, from that 1981.35 peak, the next projection called for a decline into 1985.65 which marked the end of deflation as the stage was set for a new global economic trend. Thereafter, the next two major turning points are 1989.95 and 1994.25.

December 1989, (1989.95), was the major turning point for the Japanese share market and real estate prices worldwide. In addition, it also forecast that the first stage of recession would unfold moving into a bottom in January 1991. Now that same cycle is pointing upward moving into February 1992 and, indeed, the economic numbers are just now showing that the worst of the recession is over. While the majority did not speak of recession until December 1990, our model was forecasting that the decline would unfold years in advance.

The Business Cycle and the Economic Confidence Model by Martin Armstrong

In separate research works on our Economic-Confidence Model published since 1979, the complete and detailed historical review stretching back several centuries will provide the in-depth analysis of this model for those interested in more serious study. The primary purpose of this discussion is to present an overview combined with a practical guide as to how to implement this model into your investment and/or business decision making process.

Understanding the business cycle is extremely important to successful trading, investment, and corporate strategic planning. Paul Volcker, former chairman of the Federal Reserve, stated that the business cycle frequency amounts to a duration of 8 years. Research at Princeton has revealed a similar duration of 8.6 years, but on a more dynamic scale.

The overall structure of the Princeton Economic-Confidence Model is based on an 8.6 year business cycle. This 8.6-year cycle builds in intensity to form long-waves of economic activity measuring 51.6 years. This should NOT be confused with the long- wave of Kondratieff whose work revealed an average long-wave of 54 years. Kondratieff’s work, conducted during the early part of this century, covered a period of slightly less than 150 years. At that time 40% or more of the total civil work force was employed in the agricultural sector. Therefore, the primary input used in Kondratieff’s model was the commodity sector. Today, agriculture accounts for only 3% of the total civil work force and the service sector now employs nearly 70%.

While the world waits for the Kondratieff Wave to predict the next Great Depression, the reality of the situation is quite different. The major high in commodities during the early part of this century took place in 1920 followed by the low in 1932. Precisely 54 years after 1920 provides a target of 1974 while 54 years from the 1932 low yields the target of 1986. In fact, 1974 was the major high for many commodities as 1986 was a major low. The Kondratieff Wave has come and gone and the commodity sector indeed experienced a massive deflationary wave. By 1986, only 50% of the number of farmers remained from the peak in 1974.

No one in their right mind would develop a model based on pork bellies and then claim that it’s capable of forecasting the stock market. Nevertheless, those who write so much about Kondratieff’s work are doing precisely that! If Kondratieff were alive today, he would have chosen the service industry to base his model upon rather than commodities, since services now represent the lion’s share of the economy.

Long-wave economic theory did not begin with Kondratieff. It has actually been around for centuries. Kondratieff merely captured most of the publicity during this century. We offer as one proof of this statement an illustration of a most curious chart which was published in the Wall Street Journal on February 2, 1933 with the following caption:

“The above chart [shown left] was sent to the Wall Street Journal by Edward Rogers of Detroit. Mr. Rogers states that it was found in an old desk in Philadelphia in 1902. The original drawing was much discolored. The desk was of a pattern that indicated it was at least 40 years old.

“The author of the chart is unidentified and the circumstances lead Mr. Rogers to believe that possibly the chart was made during the Civil War or before. It is submitted to Wall Street Journal subscribers for what it may be worth.”

Under the circumstances, the Wall Street Journal could not have commented on the accuracy of the chart. At that point the chart, on the surface, had predicted the past brilliantly, but what about the future? The bottom of the depression had been reached according to the stock market in 1932. However, since this factor was not clear, even at the time of publication in 1933, the Wall Street Journal was not in a position to make a qualified statement. Even though this chart accurately had pointed to all the ups and downs in the past, it could have been a forgery or a hoax that only time would reveal.

Today we have hindsight to provide us with an honest review of this chart that the most cynical skeptic cannot dispute. We know that this chart, constructed by some unknown 19th century economic explorer, was published by the Wall Street Journal during 1933 and cannot be a hoax concocted for today. Looking at the performance of this chart since 1932 yields some interesting information.

The year 1932 was indeed the bottom the Great Depression as well as the stock market. But 1934 was the real bottom in the emotional confidence of the people as they began to look toward Roosevelt for hope in his famous New Deal. The 1938 peak predicted by the chart was fairly accurate. The economy reached its peak during late 1937 to early 1938. From there, the actual bottom of the 1949 recession occurred in 1951. The chart predicted the bottom of the next recession for 1968 at which time there was a bottom of a less severe recession. The chart called for the next peak to come in 1975. In this case it was off slightly since the peak came in 1972. Then the chart predicted another decline into 1979 followed by another peak in 1983. In truth, the recession bottomed out in 1977 and the economy peaked in 1981. The chart continued to point to the next bottom in 1985.

We must admit that while not perfect, the errors tended to be less than 1 year from the actual economic events. Careful analysis of the mathematics behind this forecast from the 19th century reveals that the author made a few errors. Nonetheless, this forecast from the past illustrates that others were looking for the key to the business cycle long before 20th century man.

Another famous believer in long-wave theory was Joseph Schumpeter, a professor at Harvard. Schumpeter devoted his life to explaining long-wave theory and in the process emerged with his own Theory of Innovation. Schumpeter saw Kondratieff’s long-waves corresponding to man’s economic evolvement. For example, one wave could be attributed to the development of the railroad. That invention allowed the West and east coasts in the United States to be connected, thereby expanding the marketplace for goods and services. This enabled the East to become the center for manufacturing while the West flourished in agriculture. As prosperity unfolds, competition increases. Eventually, the peak is reached due to over-competition that results in lower profit margins. Lacking a new major innovation to allow the economic expansion to continue, the economy begins to slow and eventually a correction takes place. The wave of the 1920’s could easily be attributed in part to the development of the automobile.

Others, such as Rostow, a professor at the University of Texas, have also sought to explain Kondratieff’s long-wave. At MIT you will find another group including Jay W. Forrester who has also dedicated his life to understanding long-wave theory. At MIT they take every fundamental event and public decision and input this into their computer models.

At Princeton we have taken a different road. Our 51.6 year long-wave is not based on any of the works mentioned here, other than an agreement in the general theory that long-waves exist. We have named our model the “Economic-Confidence Model” because our research has shown that all long-waves of economic activity are NOT the same. There is a cycle of different activity in long-waves themselves. We have found that in one 51.6-year period the underlying confidence of the community may reside heavily within the public (government) sector and the private sector will have a certain degree of skepticism attached to it. The next long-wave of 51.6 years will be exactly the opposite, showing confidence moving away from government and toward the private sector. This alternating confidence of the people is caused by the excesses of each sector.

For example, during the mid 19th century, people became very skeptical about government and didn’t even trust its currency. This gave birth to the term “greenback” which referred to the only “backing” being the green ink on the reverse side of the note. To inspire the acceptance of unbacked paper currency, there used to be a schedule of interest payments on the reverse. Currency had become merely a strange form of circulating bonds.

The long-wave that resulted in the Great Depression was a wave of “Private Confidence” as people believed more in the virtues of the private sector. This high concentration of private confidence results in strong stock markets and great expansion. When it reaches its point of maximum entropy or excess, the correction begins. Due to the losses that take place, confidence then turns to government as its savior—in this case Roosevelt.

Confidence can be determined by simply monitoring capital movements. During public waves, capital is comfortable to reside in government bonds, whereas during Private Waves, capital begins to look more at diversification into stocks, commodities, business, and real estate. We have entered a new Private Wave of confidence as of July 1985. This is why the stock market continued to make new highs beyond 1986 when the bonds peaked. It is also why the ’87 crash took place, because volatility is always higher in Private Waves than in Public waves.

Many of our observations of this alternating confidence was based not merely on market activity, but on the newspaper analysis of events. Several specialized works have been published which are available through our book department for those interested in a deeper background on this subject. The titles are “The Greatest Bull Market In History” and “The Economic-Confidence Model.” Both offer a detailed account of historical events and how they correspond to this model.

As a brief introduction to the 8.6-year frequency within the Princeton Economic-Confidence Model, let us follow its course beginning with the last major panic that took place in October 1929 from the US perspective. Factoring in the month of October as .75 to represent a decimal portion of the calendar year, the calculations embark on their journey with 1929.75 to see how well the cycle will hold up in forecasting the past 52 years. The next step was to add 4.3, half the cycle duration, to come up with the next bottom. It projected 1934.05 which would have been January. This year marked the Gold Reserve Act and the beginning of the New Deal. As a result, it also marked the beginning of the turning point in that human emotion known as hope. The stock market had actually bottomed in 1932 and in the later part of 1934 it had begun a rally that would double the Dow Industrials by March of 1937. Continuing on, we apply the next half cycle of 4.3 years which brings us to the next peak projection of 1938.35. This was extremely close to the real events. The stocks had peaked early, a s they always do in a recovery. The long-term trend in the business cycle had rallied from a -38% to -10% in growth according to the Cleveland Trust Co. Index of US business activity. Despite the fact that the growth was still negative, it was a strong improvement within the economy that began to fall off reaching a -18% during 1939. The next bottom, projected out by adding another half cycle of 4.3 years to arrive at 1942.65, which corresponded to the beginning of World War II and another beginning of an economic boom. The Dow Jones Industrials had been declining since March of 1937 when it peaked at 194.40. the Dow eventually bottomed out on April 28th, 1942 at 92.92. From there the Dow would begin another 4 year rally.

The 8.6-year cycle was holding up very nicely. From 1942’s bottom, the cycle peaked again in 1946.95. This corresponded with the end of the World War II period and the beginning of the post war recession. The stock market had peaked during 1946 at the 220 level on the Dow and for the next three years the Dow traded sideways between 160 and 200.

Moving ahead, the next bottom was projected to arrive at 1951.25. The 1949 recession was a deep one in which the US did not begin to pull out until 1951. Although the business cycle began to rise due to the Korean War during mid 1950, it actually peaked during mid 1954 at a +18% on the Cleveland Trust Co. Index followed by a sharp drop to a -2% in 1954. The Dow had started to rise during 1950 and remained in a bull market rising from 195 to reach 525 by 1956.

The next cyclical peak projected out to be 1955.55. The Dow had pulled off a 250% rally between 1950 and 1956 and then fell sharply by 100 points going into 1957. The business cycle peaked during October of 1955 rising from a -2% in 1954 to a +8% growth factor during 1955. The cycle at this point appeared to hold up very nicely, being off no more than 1 year at any point.

From the 1955 projected peak, the next cyclical low was due in 1959.85. The Dow had actually bottomed during 1957. During 1958 and 1959 a bull market once again returned to the Dow Industrials. The business cycle fell from the 1955 high of a +5% to a bottom during 1958 of a -7%. Early during 1959 the business cycle growth bounced back to a +6%, but in the last quarter of 1959 fell again reaching a -1%.

The next peak on the 8.6-year cycle projected out to be 1964.15. During this year, silver coins became extinct and inflation, as measured by the CPI index, had reached 92.9 which was nearly double that of 1929. Industrial production rose in its index that year for the first time to exceed the 80 level after bottoming out during 1932 at 11.6. The Dow was still strong, reaching a high during 1964 near the 890 level only to continue to eventually reach 1001.11 during 1966.

The cyclical projection then called for a bottom on 1968.45. The Dow had peaked on February 9th, 1966 and a sharp 260 point decline had begun. Inflation had continued to mount in much of the world. The United States and six West European nations agreed on March 18th, 1968 to discontinue the sale of gold to private buyers.

The next cyclical projection pointed to a peak in 1972.75. The Dow Industrials had rallied from a sharp decline which saw the Dow bottom at 627.46 on Tuesday, May 26, 1970. From that low, the rally in the Dow peaked at 1,051.70 on January 11, 1973. That high would remain a major record high going into the 1980s. This projection was accurate because the 1973 recession was a serious one, marked by the failure of the Franklin National Bank. It would serve as the worst recession since the 1929 panic.

The next projection came up with a bottom during January 1977.05. The early peak on the Dow during 1973 was followed by a severe panic decline that dropped even below the previous cycle low in the Dow. The bottom came on December 6th, 1974 after nearly a 50% decline. Despite the fact that gold began its rally during August of 1976, the economy didn’t begin its inflationary upswing until 1977.

The next projected high on this 8.6-year cycle called for that peak to come in at 1981.35. This was the precise month when the bond market reached a bottom and interest rates began to turn downward. But, from that 1981.35 peak, the next projection called for a decline into 1985.65 which marked the end of deflation as the stage was set for a new global economic trend. Thereafter, the next two major turning points are 1989.95 and 1994.25.

December 1989, (1989.95), was the major turning point for the Japanese share market and real estate prices worldwide. In addition, it also forecast that the first stage of recession would unfold moving into a bottom in January 1991. Now that same cycle is pointing upward moving into February 1992 and, indeed, the economic numbers are just now showing that the worst of the recession is over. While the majority did not speak of recession until December 1990, our model was forecasting that the decline would unfold years in advance.

The Business Cycle and the Economic Confidence Model by Martin Armstrong

In separate research works on our Economic-Confidence Model published since 1979, the complete and detailed historical review stretching back several centuries will provide the in-depth analysis of this model for those interested in more serious study. The primary purpose of this discussion is to present an overview combined with a practical guide as to how to implement this model into your investment and/or business decision making process.

Understanding the business cycle is extremely important to successful trading, investment, and corporate strategic planning. Paul Volcker, former chairman of the Federal Reserve, stated that the business cycle frequency amounts to a duration of 8 years. Research at Princeton has revealed a similar duration of 8.6 years, but on a more dynamic scale.

The overall structure of the Princeton Economic-Confidence Model is based on an 8.6 year business cycle. This 8.6-year cycle builds in intensity to form long-waves of economic activity measuring 51.6 years. This should NOT be confused with the long- wave of Kondratieff whose work revealed an average long-wave of 54 years. Kondratieff’s work, conducted during the early part of this century, covered a period of slightly less than 150 years. At that time 40% or more of the total civil work force was employed in the agricultural sector. Therefore, the primary input used in Kondratieff’s model was the commodity sector. Today, agriculture accounts for only 3% of the total civil work force and the service sector now employs nearly 70%.

While the world waits for the Kondratieff Wave to predict the next Great Depression, the reality of the situation is quite different. The major high in commodities during the early part of this century took place in 1920 followed by the low in 1932. Precisely 54 years after 1920 provides a target of 1974 while 54 years from the 1932 low yields the target of 1986. In fact, 1974 was the major high for many commodities as 1986 was a major low. The Kondratieff Wave has come and gone and the commodity sector indeed experienced a massive deflationary wave. By 1986, only 50% of the number of farmers remained from the peak in 1974.

No one in their right mind would develop a model based on pork bellies and then claim that it’s capable of forecasting the stock market. Nevertheless, those who write so much about Kondratieff’s work are doing precisely that! If Kondratieff were alive today, he would have chosen the service industry to base his model upon rather than commodities, since services now represent the lion’s share of the economy.

Long-wave economic theory did not begin with Kondratieff. It has actually been around for centuries. Kondratieff merely captured most of the publicity during this century. We offer as one proof of this statement an illustration of a most curious chart which was published in the Wall Street Journal on February 2, 1933 with the following caption:

“The above chart [shown left] was sent to the Wall Street Journal by Edward Rogers of Detroit. Mr. Rogers states that it was found in an old desk in Philadelphia in 1902. The original drawing was much discolored. The desk was of a pattern that indicated it was at least 40 years old.

“The author of the chart is unidentified and the circumstances lead Mr. Rogers to believe that possibly the chart was made during the Civil War or before. It is submitted to Wall Street Journal subscribers for what it may be worth.”

Under the circumstances, the Wall Street Journal could not have commented on the accuracy of the chart. At that point the chart, on the surface, had predicted the past brilliantly, but what about the future? The bottom of the depression had been reached according to the stock market in 1932. However, since this factor was not clear, even at the time of publication in 1933, the Wall Street Journal was not in a position to make a qualified statement. Even though this chart accurately had pointed to all the ups and downs in the past, it could have been a forgery or a hoax that only time would reveal.

Today we have hindsight to provide us with an honest review of this chart that the most cynical skeptic cannot dispute. We know that this chart, constructed by some unknown 19th century economic explorer, was published by the Wall Street Journal during 1933 and cannot be a hoax concocted for today. Looking at the performance of this chart since 1932 yields some interesting information.

The year 1932 was indeed the bottom the Great Depression as well as the stock market. But 1934 was the real bottom in the emotional confidence of the people as they began to look toward Roosevelt for hope in his famous New Deal. The 1938 peak predicted by the chart was fairly accurate. The economy reached its peak during late 1937 to early 1938. From there, the actual bottom of the 1949 recession occurred in 1951. The chart predicted the bottom of the next recession for 1968 at which time there was a bottom of a less severe recession. The chart called for the next peak to come in 1975. In this case it was off slightly since the peak came in 1972. Then the chart predicted another decline into 1979 followed by another peak in 1983. In truth, the recession bottomed out in 1977 and the economy peaked in 1981. The chart continued to point to the next bottom in 1985.

We must admit that while not perfect, the errors tended to be less than 1 year from the actual economic events. Careful analysis of the mathematics behind this forecast from the 19th century reveals that the author made a few errors. Nonetheless, this forecast from the past illustrates that others were looking for the key to the business cycle long before 20th century man.

Another famous believer in long-wave theory was Joseph Schumpeter, a professor at Harvard. Schumpeter devoted his life to explaining long-wave theory and in the process emerged with his own Theory of Innovation. Schumpeter saw Kondratieff’s long-waves corresponding to man’s economic evolvement. For example, one wave could be attributed to the development of the railroad. That invention allowed the West and east coasts in the United States to be connected, thereby expanding the marketplace for goods and services. This enabled the East to become the center for manufacturing while the West flourished in agriculture. As prosperity unfolds, competition increases. Eventually, the peak is reached due to over-competition that results in lower profit margins. Lacking a new major innovation to allow the economic expansion to continue, the economy begins to slow and eventually a correction takes place. The wave of the 1920’s could easily be attributed in part to the development of the automobile.

Others, such as Rostow, a professor at the University of Texas, have also sought to explain Kondratieff’s long-wave. At MIT you will find another group including Jay W. Forrester who has also dedicated his life to understanding long-wave theory. At MIT they take every fundamental event and public decision and input this into their computer models.

At Princeton we have taken a different road. Our 51.6 year long-wave is not based on any of the works mentioned here, other than an agreement in the general theory that long-waves exist. We have named our model the “Economic-Confidence Model” because our research has shown that all long-waves of economic activity are NOT the same. There is a cycle of different activity in long-waves themselves. We have found that in one 51.6-year period the underlying confidence of the community may reside heavily within the public (government) sector and the private sector will have a certain degree of skepticism attached to it. The next long-wave of 51.6 years will be exactly the opposite, showing confidence moving away from government and toward the private sector. This alternating confidence of the people is caused by the excesses of each sector.

For example, during the mid 19th century, people became very skeptical about government and didn’t even trust its currency. This gave birth to the term “greenback” which referred to the only “backing” being the green ink on the reverse side of the note. To inspire the acceptance of unbacked paper currency, there used to be a schedule of interest payments on the reverse. Currency had become merely a strange form of circulating bonds.

The long-wave that resulted in the Great Depression was a wave of “Private Confidence” as people believed more in the virtues of the private sector. This high concentration of private confidence results in strong stock markets and great expansion. When it reaches its point of maximum entropy or excess, the correction begins. Due to the losses that take place, confidence then turns to government as its savior—in this case Roosevelt.

Confidence can be determined by simply monitoring capital movements. During public waves, capital is comfortable to reside in government bonds, whereas during Private Waves, capital begins to look more at diversification into stocks, commodities, business, and real estate. We have entered a new Private Wave of confidence as of July 1985. This is why the stock market continued to make new highs beyond 1986 when the bonds peaked. It is also why the ’87 crash took place, because volatility is always higher in Private Waves than in Public waves.

Many of our observations of this alternating confidence was based not merely on market activity, but on the newspaper analysis of events. Several specialized works have been published which are available through our book department for those interested in a deeper background on this subject. The titles are “The Greatest Bull Market In History” and “The Economic-Confidence Model.” Both offer a detailed account of historical events and how they correspond to this model.

Princeton’s Global Model

Princeton’s Global Model

Since the dawn of time, man has tried desperately to predict the future. Man has gazed upon the stars, summoned soothsayers and astrologers and sought guidance in the patterns of tea leaves and chicken entrails. He has studied the movements of planets, comets, and even the flight of an owl. However, no matter what methods man has tried in his attempt to pull back the curtain, which stands between the present and his destiny, nothing has ever provided the infallible key to the future.

In this age of modern wisdom, where we look back upon our forefathers as being perhaps silly and superstitious, man has failed miserably in the so-called science of economics. It has often been said that economics is the only profession where one can be perpetually wrong in his theory yet still achieve world fame and the Nobel prize.

Far too often economists seek to change “what is” into what they believe “should be”, thereby reducing the science of economics to nothing more than a corrupt political social movement. It was, after all, the conflicting economic theories of Keynes and Marx that built the Berlin Wall. While Marx was correct in identifying the source of man’s booms and busts as human nature, his error was in believing that government officials were somehow so virtuous that they were above such petty temptations or corruptions.

At Princeton, we do not consult the stars nor do we believe in trying to change human nature. If a model cannot be built on “what is” then there is no point in creating something that will “never be.” We do not subscribe to a form of economic theory that advocates government control, but believe firmly that Adam Smith was correct in his observation of the “Invisible Hand.” Through years of our own observation and money management experience, we have come to see a much more dynamic Invisible Hand at work globally that still adheres to the core principles set forth by Smith in 1776. Understanding the nature of our global economy is not that difficult once we abandon unrealistic social dreams of creating utopia. The seemingly chaotic or random behavior of our economy is due to the enormous amount of complex variables involved that determine the final outcome. Our global economy is not unlike the dynamic system of the weather where the final outcome is caused by numerous combinations of variables. A small change in just one variable, such as water temperature in the Pacific, can result in dramatic changes within the overall global weather patterns.

Another example from nature can be seen in the work of ecologists’ studies of rain forests. Science has come to understand that man cannot create a rain forest by merely planting a group of trees. There are millions of species of bacteria and insects in addition to the thousands of plants and animals that interact to form a balance within nature. Man cannot duplicate a rain forest due to his lack of knowledge concerning such a wealth of intricate variables interacting with one another to produce the final balanced system.

Another problem for man in grasping a full understanding of market and economic behavior lies in his conscious thought process. In our natural state, our mind processes and records data in a nonlinear fashion. When we meet someone special, perhaps in a restaurant, our subconscious mind records the music and setting of the moment. It is quietly observing what the other person is wearing, the color of the table cloth, the flicker of candlelight, the background music and so on. Our conscious mind focuses on the conversation at hand. Months or even years later, if we hear that particular background music our mind suddenly retrieves the experience and consciously we relive the event right down to the twinkle of candlelight.

Economic and market behavior is quite similar to the operation of our mind. There are numerous variables hidden within the equation that determine the end result. Consciously we focus on only a small fraction of the variables involved. For example, we may pay a lot of attention to interest rates and stock market behavior or unemployment and its influence upon interest rates. We then try to interpret and make a judgment as to what the trend will be based upon just a handful of simplistic, fundamental relationships. Inevitably, such analysis proves to be incorrect due to the lack of attention paid to the wealth of other variables that will influence the final outcome. Normally, our subconscious mind would record these types of things for us in a social setting. Yet, in financial analysis we are ignoring the actual process of collecting knowledge by continually trying to reduce the entire fate of the world down to a few simplistic relationships such as interest rates, trade, corporate profits, or whatever.

We strive to develop a global model which filters in all key economic data along with free market movements that include everything from bonds and stocks to wheat and aluminum. The results, thus far, have given us perhaps the best track record of long-term economic forecasts on a consistent basis. Our overall model design takes into account 35 world economies and views the global trend as a sum of the parts.

In a study we published in 1986 entitled The Greatest Bull Market In History, a complete review of the world economy is given for the period of 1919 to 1946. Both the bull market and the great crash are covered in detail showing the precise interaction between all major commodities, stock and bond markets, foreign exchange, government decisions, corporate profits, unemployment and gross national product. By putting the global economy together, rather than attempting to forecast the fate of one market or economy in isolation, a new level of understanding emerges. For every action taken in Germany or France, a reaction takes place in all other nations ranging from subtle changes to major disruptions.

The global trends that are set in motion are the result of smaller trends emerging from every economy around the world. All nations strive for a trade surplus. However, it is impossible for one nation to enjoy a trade surplus unless someone else endures a trade deficit. Correspondingly, it is impossible for the entire world to experience prosperity simultaneously. One nation’s boom has often been another’s bust.

As a result of the two world wars, the United States emerged as the wealthiest nation on earth holding 76% of the free world’s gold reserves. As the countries of Europe fought each other, capital fled to the United States and created jobs and expanded its manufacturing base. However, as the US adopted a more socialistic philosophy by driving corporate taxes to 70% and the top personal income tax to 90% during the 1960s, capital fled offshore in a stampede. To this day, 60% of the US trade deficit is made up of US companies manufacturing their own goods offshore.

The trends in international capital movement are set in motion by the forces of taxation, inflation, geopolitical and financial security, foreign exchange, and the cost of labor. There are some additional minor influences, such as interest rate differentials. Nevertheless, capital is continually flowing from one economy to another in search of profit and/or financial stability. With the advent of floating exchange rates, this one factor above all others has become the primary source for volatility and capital flow movement. Price swings of 30-40% in the course of 1 to 2 years can wipe out normal profit margins and simple interest rate differentials.

Examples of the influence of foreign exchange can be extracted from virtually any commodity or stock market. If we look at gold we can see that the bull market moving into 1980 was a true bull market since gold made new highs in terms of every world currency. However, gold bottomed in 1985 in terms of dollars and rallied to $500 going into 1987 (Figure #1). While most proclaimed this to be a new bull market, gold was still declining in terms of most other currencies. In order to create a bull market, it takes solid buying support from all nations—not just one. If we look at the Dow Jones Industrials since 1915 expressed in Swiss francs (Figure #2), we can see that by 1991 we had only risen to re-test the true peak in this market established back in 1966. Capital has only begun to return since the tax structure in the United States was drastically reduced. The true definition of a bull market is a market that rises in ALL forms of currency, NOT just one. When expressed in terms of a basket of currencies gold peaked in 1986, not 1987 (Figure #3).

At Princeton, we have built global models by gathering together the world’s largest database of capital markets. Our computer models have every world currency back to 1900 with major currencies back to the 1700s. We have the most complete database of world stock markets, interest rates and commodities combined with most economic indicators. Using this immense foundation of data we have also built one of the few true Artificial Intelligence computer models. Unlike expert systems where man merely inserts his own rules, true Artificial Intelligence systems learn through experience. Our computer model has taken every individual variable and tracked it side by side with everything else in the global economy. Its forecasts are the result of history —not theory!

Man can only forecast what he believes is possible. If he has never experienced war, how can he possibly forecast war? The global approach to forecasting is the only hope we have of fully understanding the complex network of global interrelationships. For every fundamental that we believe moves the market, there is an example of the same fundamental producing the opposite result. Knowing when higher interest rates affect the stock market and when they do not, results from the external influences we may not be watching very closely.

For every up-trend there is always the inevitable downtrend. When the marketplace moves in the opposite direction of what everyone expects, it is not the markets that are wrong—it is our frail and inept interpretations. No one will ever be able to forecast the future based upon opinion. The only reasonable approach is an unbiased one that considers all the possibilities based upon research of “what is” rather than “what ought to be.”

Since the dawn of time, man has tried desperately to predict the future. Man has gazed upon the stars, summoned soothsayers and astrologers and sought guidance in the patterns of tea leaves and chicken entrails. He has studied the movements of planets, comets, and even the flight of an owl. However, no matter what methods man has tried in his attempt to pull back the curtain, which stands between the present and his destiny, nothing has ever provided the infallible key to the future.

In this age of modern wisdom, where we look back upon our forefathers as being perhaps silly and superstitious, man has failed miserably in the so-called science of economics. It has often been said that economics is the only profession where one can be perpetually wrong in his theory yet still achieve world fame and the Nobel prize.

Far too often economists seek to change “what is” into what they believe “should be”, thereby reducing the science of economics to nothing more than a corrupt political social movement. It was, after all, the conflicting economic theories of Keynes and Marx that built the Berlin Wall. While Marx was correct in identifying the source of man’s booms and busts as human nature, his error was in believing that government officials were somehow so virtuous that they were above such petty temptations or corruptions.

At Princeton, we do not consult the stars nor do we believe in trying to change human nature. If a model cannot be built on “what is” then there is no point in creating something that will “never be.” We do not subscribe to a form of economic theory that advocates government control, but believe firmly that Adam Smith was correct in his observation of the “Invisible Hand.” Through years of our own observation and money management experience, we have come to see a much more dynamic Invisible Hand at work globally that still adheres to the core principles set forth by Smith in 1776. Understanding the nature of our global economy is not that difficult once we abandon unrealistic social dreams of creating utopia. The seemingly chaotic or random behavior of our economy is due to the enormous amount of complex variables involved that determine the final outcome. Our global economy is not unlike the dynamic system of the weather where the final outcome is caused by numerous combinations of variables. A small change in just one variable, such as water temperature in the Pacific, can result in dramatic changes within the overall global weather patterns.

Another example from nature can be seen in the work of ecologists’ studies of rain forests. Science has come to understand that man cannot create a rain forest by merely planting a group of trees. There are millions of species of bacteria and insects in addition to the thousands of plants and animals that interact to form a balance within nature. Man cannot duplicate a rain forest due to his lack of knowledge concerning such a wealth of intricate variables interacting with one another to produce the final balanced system.

Another problem for man in grasping a full understanding of market and economic behavior lies in his conscious thought process. In our natural state, our mind processes and records data in a nonlinear fashion. When we meet someone special, perhaps in a restaurant, our subconscious mind records the music and setting of the moment. It is quietly observing what the other person is wearing, the color of the table cloth, the flicker of candlelight, the background music and so on. Our conscious mind focuses on the conversation at hand. Months or even years later, if we hear that particular background music our mind suddenly retrieves the experience and consciously we relive the event right down to the twinkle of candlelight.

Economic and market behavior is quite similar to the operation of our mind. There are numerous variables hidden within the equation that determine the end result. Consciously we focus on only a small fraction of the variables involved. For example, we may pay a lot of attention to interest rates and stock market behavior or unemployment and its influence upon interest rates. We then try to interpret and make a judgment as to what the trend will be based upon just a handful of simplistic, fundamental relationships. Inevitably, such analysis proves to be incorrect due to the lack of attention paid to the wealth of other variables that will influence the final outcome. Normally, our subconscious mind would record these types of things for us in a social setting. Yet, in financial analysis we are ignoring the actual process of collecting knowledge by continually trying to reduce the entire fate of the world down to a few simplistic relationships such as interest rates, trade, corporate profits, or whatever.

We strive to develop a global model which filters in all key economic data along with free market movements that include everything from bonds and stocks to wheat and aluminum. The results, thus far, have given us perhaps the best track record of long-term economic forecasts on a consistent basis. Our overall model design takes into account 35 world economies and views the global trend as a sum of the parts.

In a study we published in 1986 entitled The Greatest Bull Market In History, a complete review of the world economy is given for the period of 1919 to 1946. Both the bull market and the great crash are covered in detail showing the precise interaction between all major commodities, stock and bond markets, foreign exchange, government decisions, corporate profits, unemployment and gross national product. By putting the global economy together, rather than attempting to forecast the fate of one market or economy in isolation, a new level of understanding emerges. For every action taken in Germany or France, a reaction takes place in all other nations ranging from subtle changes to major disruptions.

The global trends that are set in motion are the result of smaller trends emerging from every economy around the world. All nations strive for a trade surplus. However, it is impossible for one nation to enjoy a trade surplus unless someone else endures a trade deficit. Correspondingly, it is impossible for the entire world to experience prosperity simultaneously. One nation’s boom has often been another’s bust.

As a result of the two world wars, the United States emerged as the wealthiest nation on earth holding 76% of the free world’s gold reserves. As the countries of Europe fought each other, capital fled to the United States and created jobs and expanded its manufacturing base. However, as the US adopted a more socialistic philosophy by driving corporate taxes to 70% and the top personal income tax to 90% during the 1960s, capital fled offshore in a stampede. To this day, 60% of the US trade deficit is made up of US companies manufacturing their own goods offshore.

The trends in international capital movement are set in motion by the forces of taxation, inflation, geopolitical and financial security, foreign exchange, and the cost of labor. There are some additional minor influences, such as interest rate differentials. Nevertheless, capital is continually flowing from one economy to another in search of profit and/or financial stability. With the advent of floating exchange rates, this one factor above all others has become the primary source for volatility and capital flow movement. Price swings of 30-40% in the course of 1 to 2 years can wipe out normal profit margins and simple interest rate differentials.

Examples of the influence of foreign exchange can be extracted from virtually any commodity or stock market. If we look at gold we can see that the bull market moving into 1980 was a true bull market since gold made new highs in terms of every world currency. However, gold bottomed in 1985 in terms of dollars and rallied to $500 going into 1987 (Figure #1). While most proclaimed this to be a new bull market, gold was still declining in terms of most other currencies. In order to create a bull market, it takes solid buying support from all nations—not just one. If we look at the Dow Jones Industrials since 1915 expressed in Swiss francs (Figure #2), we can see that by 1991 we had only risen to re-test the true peak in this market established back in 1966. Capital has only begun to return since the tax structure in the United States was drastically reduced. The true definition of a bull market is a market that rises in ALL forms of currency, NOT just one. When expressed in terms of a basket of currencies gold peaked in 1986, not 1987 (Figure #3).

At Princeton, we have built global models by gathering together the world’s largest database of capital markets. Our computer models have every world currency back to 1900 with major currencies back to the 1700s. We have the most complete database of world stock markets, interest rates and commodities combined with most economic indicators. Using this immense foundation of data we have also built one of the few true Artificial Intelligence computer models. Unlike expert systems where man merely inserts his own rules, true Artificial Intelligence systems learn through experience. Our computer model has taken every individual variable and tracked it side by side with everything else in the global economy. Its forecasts are the result of history —not theory!

Man can only forecast what he believes is possible. If he has never experienced war, how can he possibly forecast war? The global approach to forecasting is the only hope we have of fully understanding the complex network of global interrelationships. For every fundamental that we believe moves the market, there is an example of the same fundamental producing the opposite result. Knowing when higher interest rates affect the stock market and when they do not, results from the external influences we may not be watching very closely.

For every up-trend there is always the inevitable downtrend. When the marketplace moves in the opposite direction of what everyone expects, it is not the markets that are wrong—it is our frail and inept interpretations. No one will ever be able to forecast the future based upon opinion. The only reasonable approach is an unbiased one that considers all the possibilities based upon research of “what is” rather than “what ought to be.”

PEI AI computer models

Artificial Intelligence Computer Models

Forecasting the World Princeton-Tokyo-London-Sydney-Hong Kong